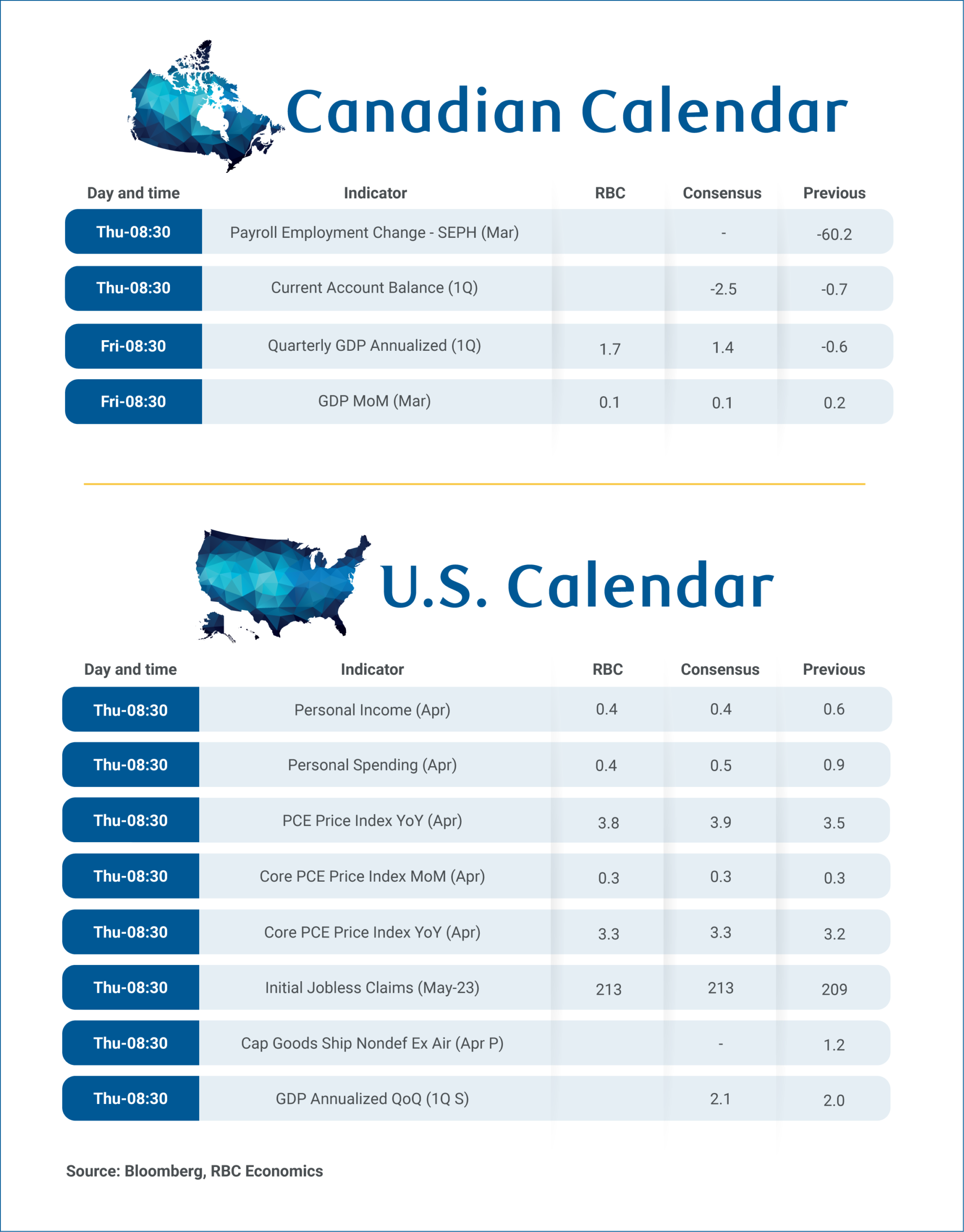

Canada’s economy likely returned to growth in Q1 2026 with gross domestic product bouncing back by an annualized 1.7% after declining 0.6% in Q4, supported by improving domestic growth drivers.

Details behind the decline in Q4 were less concerning than headlines—domestic demand improved with governments, consumers, and businesses all increasing spending while the offset mainly come from using up inventories, and another decline in residential investment.

Residential investment will remain a soft spot in Q1 with home resales continuing to decline, but household and government spending have both been picking up and a large inventory subtraction in Q4 is unlikely to be repeated.

A surge in Q1 imports could leave net exports subtracting about 4 percentage points from growth, but that’s also consistent with firming consumer spending and business investment. Temporary disruptions from large strikes in the education and transportation (postal) sectors subtracted from Q4 growth, but will add to Q1 output with workers back on the job.

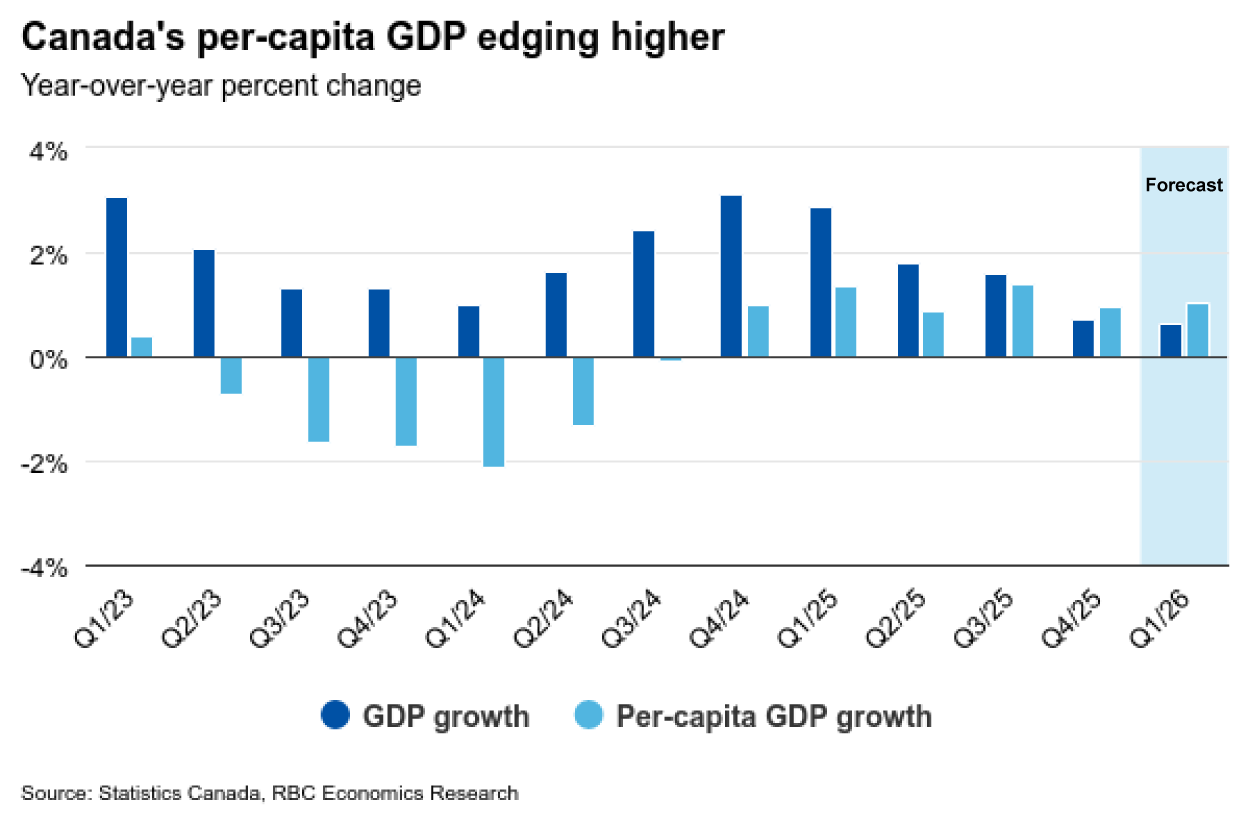

Broadly, the 1.7% quarterly annualized growth in Q1 was again against a backdrop of rapidly slowing immigration and population growth. By our count, interpolating recent demographic trends (specifically a declining non-permanent resident population) would suggest little change in overall population in Q1, and further acceleration in per capita economic growth.

This remains consistent with our overall expectation that per person economic conditions in Canada should continue to improve in 2026 after rising in 2025 for the first time in three years. That is, however, contingent on key assumptions that oil prices start to normalize beyond this quarter, and broader U.S. tariffs won’t escalate.

Monthly GDP points to modest increase in March

We expect GDP to have continued to grow in March, expanding 0.1% from February in real terms after advancing at an average pace of 0.15% in the previous two months. That’s above Statistics Canada’s preliminary estimate from a month ago calling for a flat reading in March.

Growth was led by wholesale sales, particularly in the machinery, equipment and supplies subsector, reflecting increased deliveries to government clients. Manufacturing output also rose, supported by an ongoing recovery in the auto sector after earlier disruptions. Those gains were offset partially by contracting mining and oil and gas extraction output and weaker retail activities in March.

Canada’s March Survey of Employment, Payrolls and Hours (SEPH) will be watched closely after a sharp drop in jobs in the timelier Labour Force Survey (LFS) in 2026 to April. SEPH employment counts have been persistently lagging paid employment counts in the LFS (unchanged from a year ago as of February in SEPH versus a 0.4% increase in the LFS). Still, job vacancies in the SEPH (not available from the LFS) have been edging higher in a sign labour demand is stabilizing. We expect SEPH wage growth will continue to underperform surprisingly firm LFS readings in recent months. SEPH wage growth has been running around 3%, which is more consistent with an elevated unemployment rate vs. the 4.5% plus readings from the LFS in March and April.

We expect personal income and spending to have both risen 0.4% in April in the U.S. from March, the latter entirely reflecting a surge in prices led by gasoline, while real spending declined 0.1%.