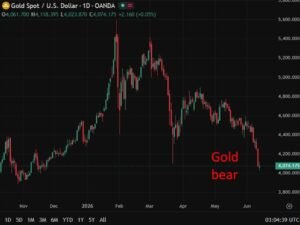

Georgia’s latest purchase is a small but illustrative example of a much larger global trend, with central banks buying over 970 tons of gold in the first quarter alone, close to 80% of all 2025 purchases. This demand has shown low price sensitivity, reinforcing a structural floor under gold prices regardless of near term moves. With Ukraine, Middle East tensions and the ongoing US-Iran conflict feeding a persistent risk premium, gold’s safe haven appeal looks set to remain elevated, likely limiting downside even during periods of broader risk appetite while amplifying gains during acute escalation phases.

—

Georgia’s central bank bought another $100mn in gold, lifting reserves to a record $7bn, as global central banks bought 970 tons in Q1 alone.

Summary:

- The National Bank of Georgia purchased an additional $100mn worth of LBMA standard gold bars for its international reserves, lifting the share of monetary gold in reserves to 15.5% and pushing total reserves to a record $7.0bn, equivalent to 114.8% of the IMF’s reserve adequacy metric

- Central banks worldwide purchased over 970 tons of gold in the first quarter of 2026 alone, representing approximately 80% of total 2025 acquisitions of 1,235 tons, with annual purchases exceeding 1,000 tons for four consecutive years from 2022 to 2025

- Central bank gold demand exhibits low price sensitivity, which mainly supports the stability of the gold price floor

- The conflict in Ukraine, escalating Middle East tensions, US-China trade frictions and the US-Iran conflict that began in February 2026 have collectively reinforced a structural risk premium in gold pricing, elevating its enduring value as a safe haven asset

The National Bank of Georgia has purchased an additional $100mn worth of highest purity gold bars for its international reserves, lifting the share of monetary gold in its reserves to 15.5% and pushing total reserves to a record $7.0bn, equivalent to 114.8% of the IMF’s reserve adequacy benchmark.

The move is part of Georgia’s broader reserve diversification strategy, but it also reflects a much larger global pattern. Central banks worldwide purchased over 970 tons of gold in the first quarter of 2026 alone, representing roughly 80% of total acquisitions across all of 2025, which itself totalled 1,235 tons. Aggregate annual central bank gold purchases have now exceeded 1,000 tons for four consecutive years, from 2022 through 2025.

A defining feature of this demand is its low sensitivity to price. Central banks have continued accumulating gold regardless of where prices stand, a dynamic that primarily supports and stabilises a price floor for the metal rather than amplifying short term swings.

Underpinning this sustained buying is a broader set of geopolitical pressures. The ongoing conflict in Ukraine, escalating tensions across the Middle East, persistent US-China trade frictions, and the US-Iran conflict that began in February 2026 have together reinforced a structural risk premium embedded in gold pricing, cementing its role as an enduring safe haven asset for reserve managers navigating an increasingly fractured global landscape.