- The ECB hiked policy rates by 25bp as expected, bringing the deposit rate to 2.25% at the June meeting.

- Lagarde highlighted the robustness of the decision to hike rates across a range of scenarios, downplayed growth risks, and emphasised upside risks to the inflation outlook.

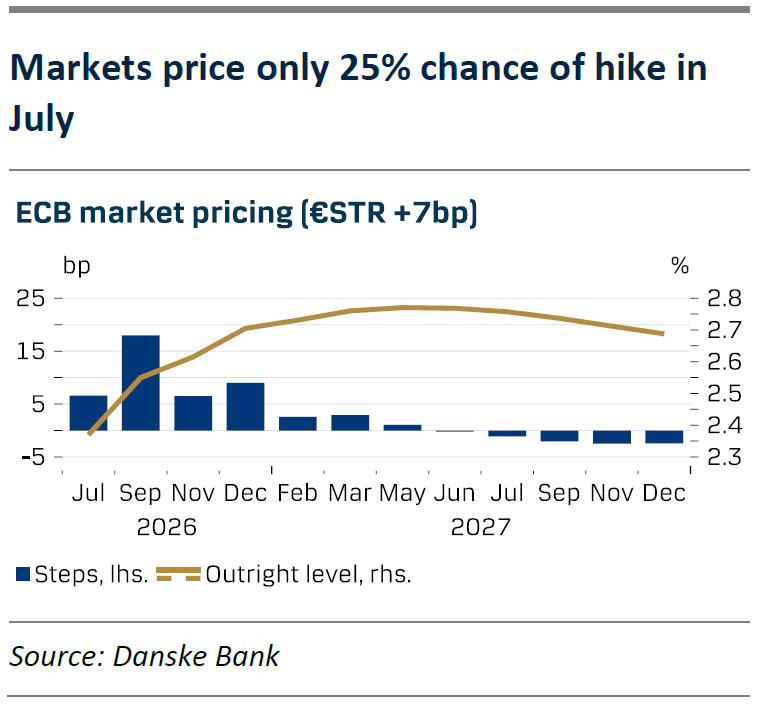

- We now expect the ECB to deliver its second hike in September (prev. July). We maintain our call for two cuts in H1 2027.

For the first time since September 2023, the ECB hiked its policy rates by 25bp, bringing the deposit rate to 2.25%. The decision was motivated by the war in the Middle East “generating inflation pressures” highlighting that “the decision to raise rates is robust across a range of scenarios mapping out how the shock might evolve and affect the medium-term outlook for the euro area.” Even in a “mild scenario” where energy prices decline significantly more than implied by current futures, inflation is expected to average 1.8% y/y in both 2027 and 2028 with core inflation above 2%. With a primary objective of maintaining price stability, the ECB are thereby assessing that monetary policy needs to be tightened.

The market reacted to the new staff projections by sending European yields higher as the new staff projections showed higher inflation but only slightly lower growth (see chart). For 2026, GDP growth is seen at 0.8% y/y (from: 0.9%) and inflation at 3.0% y/y (from: 2.6%) with core at 2.5% (from: 2.3% y/y). As euro area GDP fell 0.2 % q/q in Q1 due to distortions of the Irish export data the ECB staff decided to use a modified measure of GDP for Ireland reflecting only domestic demand. For this reason, GDP growth is holding up much better than we had anticipated based on the “official” measure of GDP. As the staff projections include market expectations of around 75bp worth of hikes and only then see inflation back at 2.0% in 2028 while growth is still holding up relatively well, we expect the ECB to deliver a second hike. However, as we also expect growth to disappoint relative to their expectations even on the modified measure, we do not expect more than two hikes to be delivered.

During the press conference, Lagarde repeatedly highlighted that this was not simply an “insurance” hike and that the interest rate decision was robust across the four scenarios, which now also includes a “milder scenario” to reflect the two-sided risk picture. While highlighting that some measures of underlying inflation had increased, the ECB was confident that they were not seeing second round effects yet, while also downplaying the importance of the latest high services reading in May. This led markets to push European rates back to levels prior to the decision.

To us, it was striking how little downside risks to the growth outlook were mentioned given the weakness that has already been evident across various measures the past months. Lagarde repeatedly emphasized that the ECB has a “price stability mandate” to mitigate a broadening of the energy shock. She said that the main risk to growth would be the ECB not taking a decision to hike as inflation would then increase too much thereby prompting an even large tightening later. This confirms the ECB’s bias towards curbing upside inflation risks rather than addressing downside growth risks, which is one reason for why we expect another 25bp hike.

We update our ECB call and now expect the ECB to deliver its second hike in September (prev. July). Growth data has disappointed lately and wage growth is falling faster than expected. At the same time, the energy shock is propagating at a normal speed which gives the ECB more time to assess any indirect and second-round effects before embarking on a second hike. Ahead of the July meeting, there will also be limited further data releases with only one inflation release for July and one official PMI release, although the GC will likely also have access to the July report. The wait-and-see approach in July was also confirmed in sources stories following the press conference.

We emphasize the risk that ECB might deliver the second hike already in July if the war in Iran escalates or the increase in services inflation we saw in May was indeed not due to an idiosyncratic factor related to seasonality but a more broad-based pickup in inflation. We stress that the decision of a hike in July or September does not significantly affect the economic outlook nor our overall view on rates markets where we still favour playing the move for lower short-end swap rates.