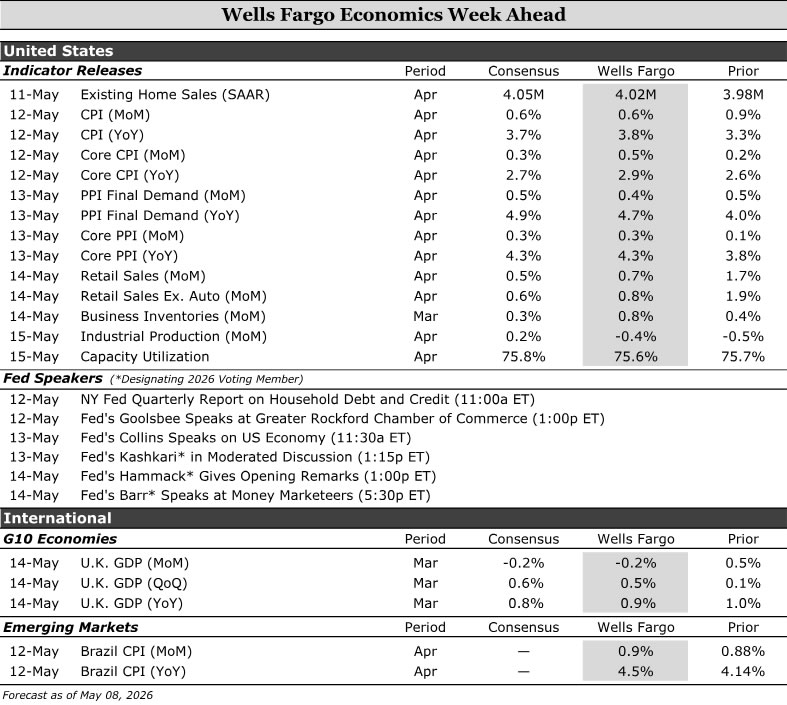

U.S. inflation data are set to firm modestly in April, with headline CPI rising toward 3.8% year-over-year and core holding near 2.9%, reflecting energy‑related pressures spilling into food, services and some goods even as shelter inflation continues to cool. Retail sales, meanwhile, are likely to show headline growth of about 0.7% month-over-month, but largely due to higher prices rather than stronger volumes, pointing to steady but increasingly price‑constrained consumer demand. In the UK, growth appears to be cooling after early‑quarter strength, with Q1 GDP tracking around 0.5%, consistent with a slowing but still stable economy and reinforcing the Bank of England’s cautious, data‑dependent stance. In Brazil, inflation is picking up more decisively, with April IPCA inflation near 0.9% month-over-month and around 4.5% year-over-year, highlighting rising energy and food pressures that complicate, but do not yet derail, a still‑cautious path toward policy easing.

United States:

- CPI (Tuesday), Retail Sales (Thursday)

G10 Economies:

Emerging Markets:

U.S. Week Ahead

CPI • Tuesday

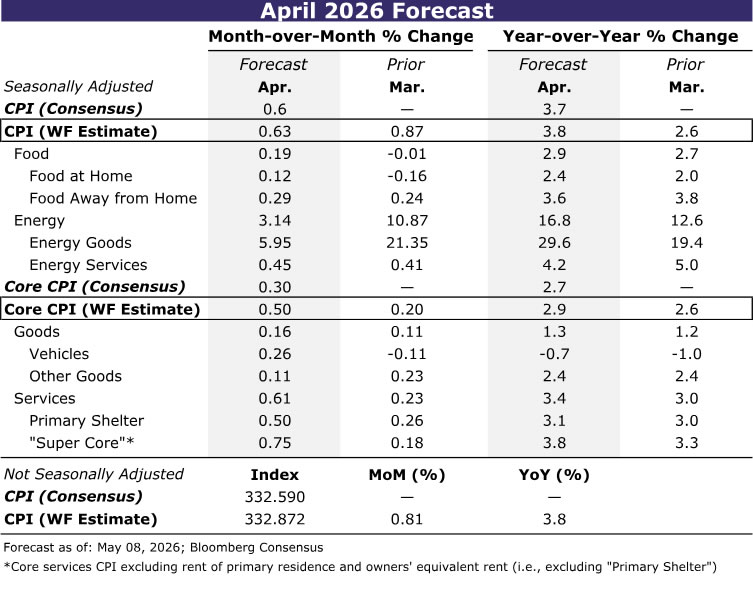

April’s CPI report will be more interesting than usual. The ongoing conflict in the Middle East has kept energy prices elevated, which will start to generate more obvious spillovers into other areas of inflation. We estimate headline CPI to rise 0.63% over the month, lifting the year-over-year pace to 3.8%.

Energy goods are poised for a 6% monthly gain as the jump in crude oil prices continues to pass through to the pump. Food at home is likely to accelerate after March’s pullback, with grocery prices set to strengthen later this year amid rising transportation costs and higher fuel and fertilizer input prices.

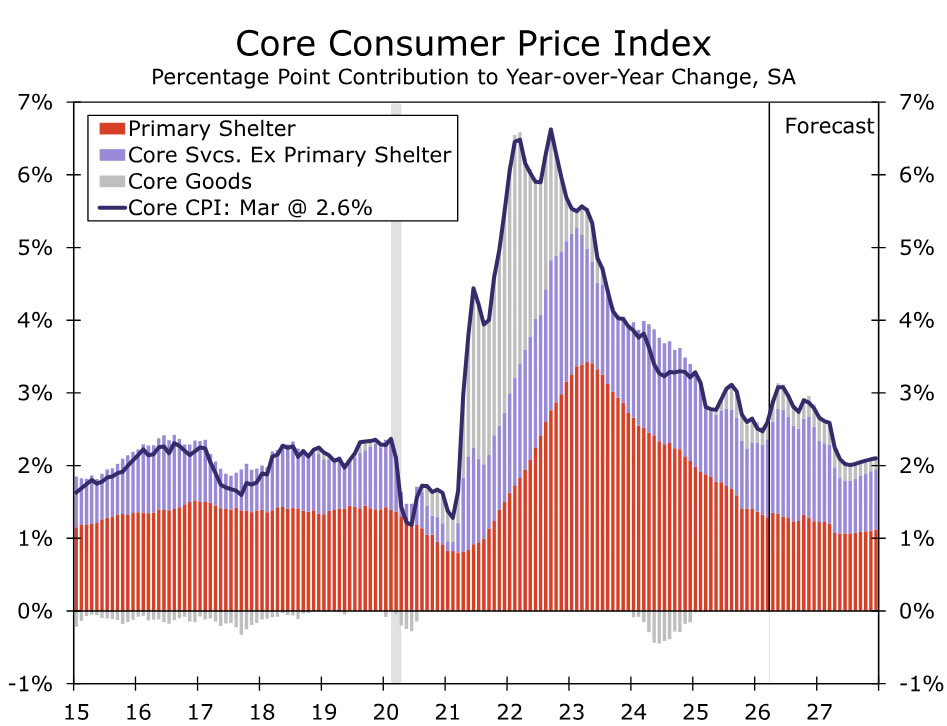

Excluding food and energy, we look for core CPI to increase 0.50% in April and 2.9% on a year-ago basis. The monthly pop is expected to be driven by core services, where strength will be partly—but not entirely—a mirage. The unwinding of a government shutdown-related survey quirk is expected to lead primary shelter to increase at twice its recent pace. We expect shelter inflation to quickly resume its moderation in May though, as real-time rent measures point to further softening. Excluding shelter, services should be genuinely hot thanks to higher jet fuel costs leading to a jump in airfares.

Meantime, a rebound in used vehicle prices will boost core goods inflation, though price growth for other core goods is likely to cool following March’s out-sized gains in apparel and recreational goods.

Looking ahead, we continue to forecast the year‑over‑year rate of core CPI to remain stuck close to 3.0% this year. Shelter inflation should continue to cool, but progress elsewhere is proving harder to come by. At the same time, slowing wage growth has weighed on consumer purchasing power and will likely limit firms’ ability to pass along higher costs. That should help temper broader inflation by year-end even as underlying pressures remain firm.

Retail Sales • Thursday

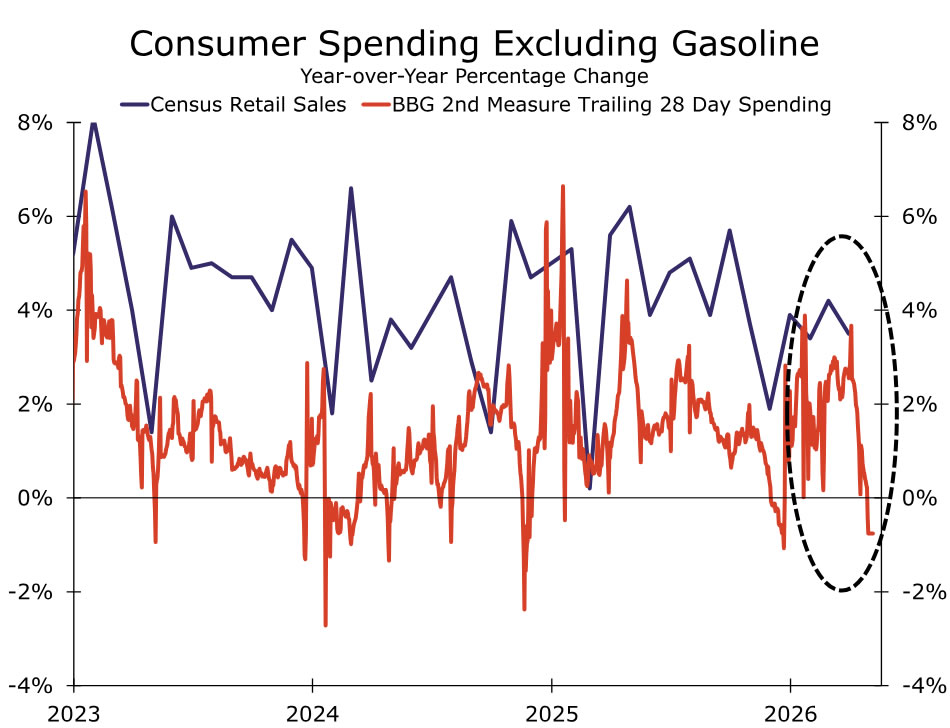

April retail sales data will be misleading at first glance as they will largely reflect higher prices rather than volumes. The data are reported nominally, thus not adjusted for inflation. While we forecast total retail sales rose 0.7% last month, after accounting for an around 0.7% gain in consumer goods prices, real retail sales were likely much weaker, potentially negative.

That’s the signal we’re getting from high-frequency credit card data, where spending outside gasoline collapsed last month (chart). While more volatile, the card data track decently well with the contours of retail spending.

The spending environment has ultimately grown more challenging as higher gas prices weigh on consumer purchasing power. Real household income, excluding transfer payments like unemployment benefits and social security, has trended lower and now turned modestly negative on a year-ago basis, signaling that compensation remains a key risk to households’ ability to spend ahead. Consumers are saving less as a result to keep spending, and they’re also relying on credit and/or their balance sheets. This all suggests a slower spending environment ahead.

G10 Week Ahead

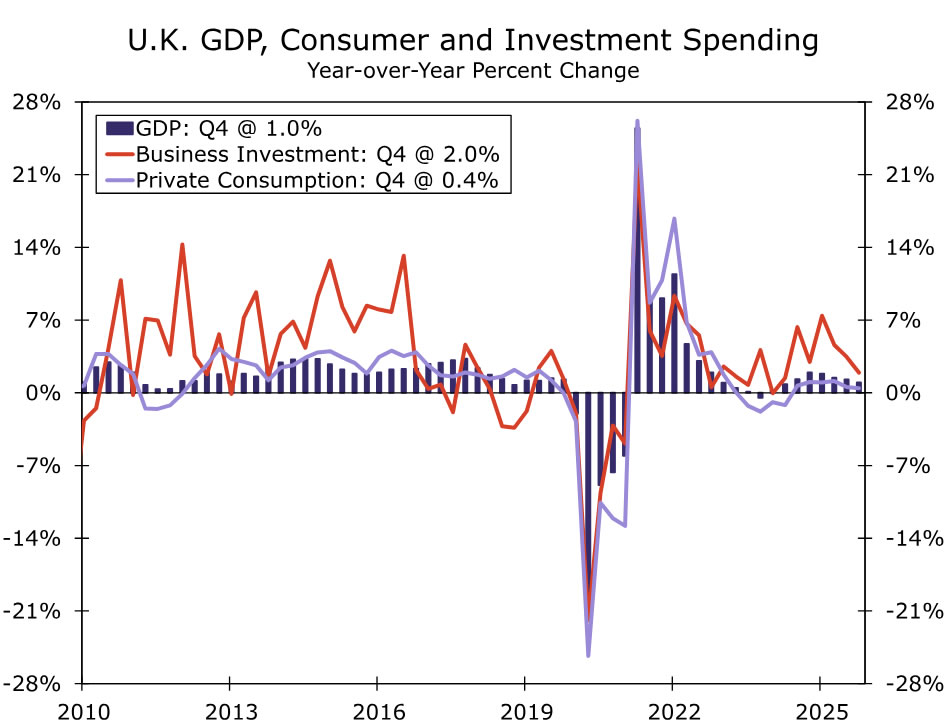

U.K. GDP • Thursday

Next week brings the release of UK GDP data for March and Q1-2026. February growth surprised to the upside, with output rising 0.5% month-over-month (aside from manufacturing). For March, we expect GDP to contract by around 0.2%. That would still leave Q1 growth at 0.5%, in line with Bank of England (BoE) recent projections.

March PMIs were weak across manufacturing and services, reflecting softer sentiment and elevated uncertainty tied to the war in the Middle East. Construction was the exception, though that was supported by energy-related demand and a return to more typical weather conditions after February’s unusually wet weather.

Against this backdrop, the BoE’s recent 8–1 vote to hold the Bank Rate at 3.75% struck us as broadly balanced with a slight hawkish lean. Greater emphasis on scenario-based forecasts highlighted optionality rather than a single outlook, while growth concerns partly offset inflation risks. As such, an upside GDP surprise next week would likely be treated cautiously, especially as anecdotal evidence suggests household and business activity may have been pulled forward, which could have boosted late‑March data and skewed risks to the upside. A weaker print would reinforce the Bank’s wait-and-see stance. That said, rising fertilizer prices and persistently high energy costs increase the risk of second-round inflation effects. We have therefore revised our Bank Rate outlook to include two hikes this year, up from a baseline of no changes. While uncertainty remains high and tied to developments in the Middle East, even with a rapid resolution, at least one hike may be needed to prevent second-round effects from becoming entrenched.

EM Week Ahead

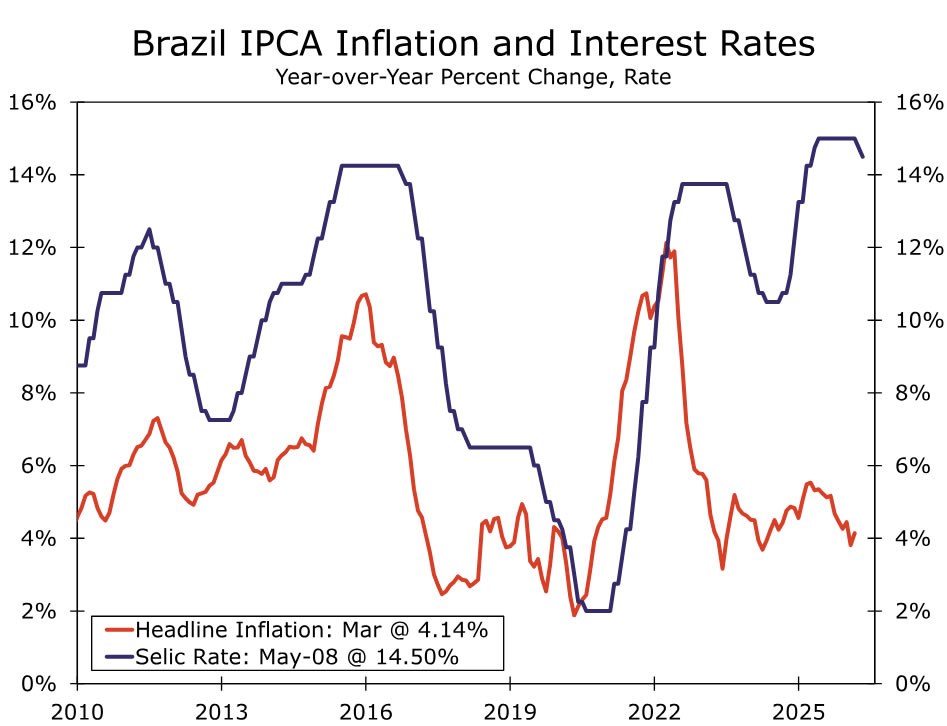

Brazil IPCA • Tuesday

We expect Brazil’s April IPCA to rise a sharp 0.9% month-over-month, pushing headline inflation to around or slightly above the top of the target band at 4.5% year-over-year. Energy remains the key near‑term upside risk, with the Middle East conflict lingering and physical supply constraints becoming more binding, driving stronger pass‑through into refined products. Food inflation was already firming in March, and higher transport and fertilizer costs should broaden price pressures across food categories in coming months.

While core inflation remains restrained by restrictive real rates, administrative price smoothing and fiscal offsets, particularly in an election year, are adding upside risks to inflation expectations. Median 2026 expectations have risen to 4.9% from 3.9% prior to the US‑Iran war, per the Brazilian Central Bank’s (BCB) FOCUS Survey. Against this backdrop, we think the BCB is likely to proceed with a cautious cut at the June meeting, but the outlook beyond that has become increasingly uncertain, with a pause in the easing cycle looking more likely.