Canada’s economy had a soft start to 2026. Real GDP growth disappointed consensus expectations and was broadly unchanged in Q1 and the unemployment rate has edged higher.

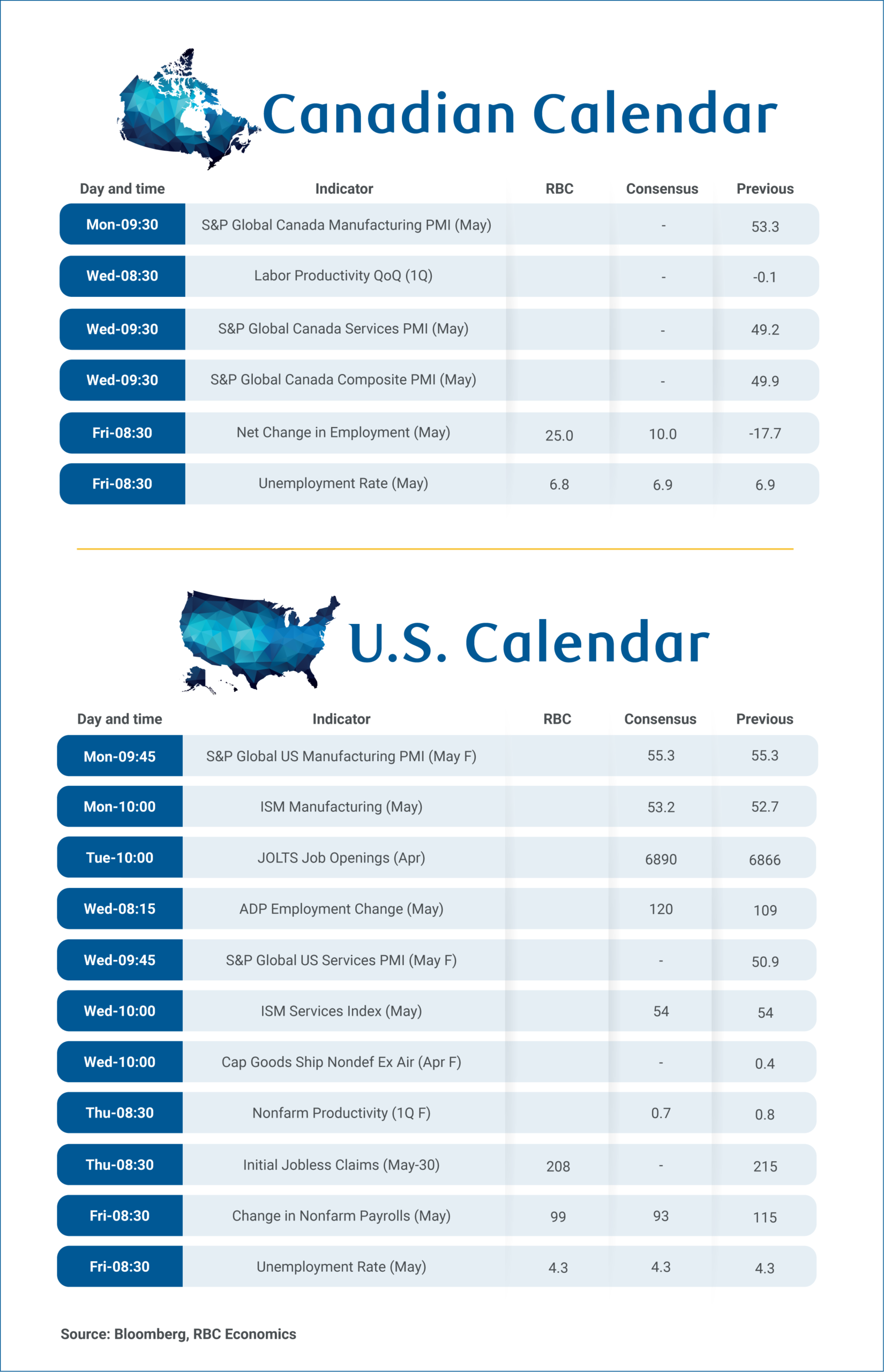

Still, we expect signs of stabilizing labour demand in the summer and hiring for the federal government census (typically 15,000 jobs) to have driven moderate job growth of about 25,000 in May, while the unemployment rate likely ticked lower to 6.8%.

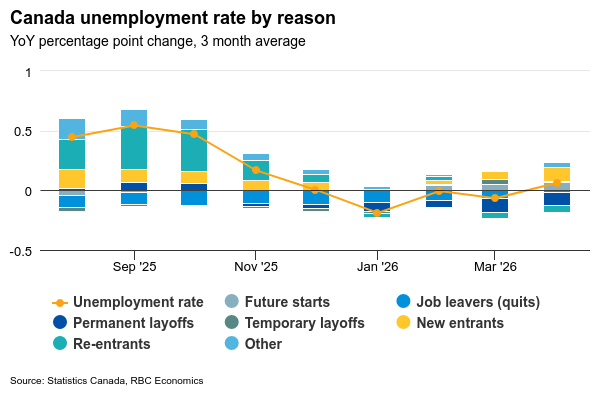

This improvement follows large counts of job losses earlier this year, but also hidden signs of resilience in the labour market. Critically, layoffs have been limited to heavily trade exposed sectors, and have been declining in total since October 2025. Instead, unemployment increases in 2026 largely reflected longer job searches for new market entrants due to persistently weak hiring.

That is little comfort for those looking for work, but it’s not the kind of labour market softening typically seen, for example, at the beginning of a recession.

In a recent speech, the Bank of Canada’s Deputy Governor Nicolas Vincent also characterized the job market as “low hire, low fire,” and highlighted a high share of people that have been out of work for a long time, and particularly high unemployment among young job seekers.

Overall, hiring intentions took a step back after the Middle East conflict injected new uncertainty into the business operating environment. Total job postings on Indeed.com, however, showed signs of resilience, with job postings starting to bounce back in May after declining in March and April.

Looking ahead, elevated oil prices remain a key risk to the Canadian economy and labour market. Sharply higher oil prices raise revenue flowing into oil producing regions, but could also divert business priorities from hiring toward margin preservation as fuel costs surge.

Meanwhile, concerns about consumer demand (with higher gasoline prices cutting into household purchasing power) could also limit businesses’ ability to pass on those cost increases while remaining competitive. Though, early consumer spending data show limited signs of demand destruction so far.

We will continue to monitor conditions as elevated oil prices persist. However, with household demand broadly holding up right now, our base case forecast remains cautiously optimistic for more stabilization in hiring in the summer, and a gradual decline in the unemployment rate toward the end of this year.

We expect structural tightness in the U.S. labour market to have persisted in May, with the unemployment rate holding steady at a decade-low 4.3% while jobs grew 99k to broadly match the 115k pace in April. Average hourly earnings are expected to have accelerated, rising 0.3% in May. Initial claims likely held low, at 208k vs. the 215k reported this week.