Canadian Highlights

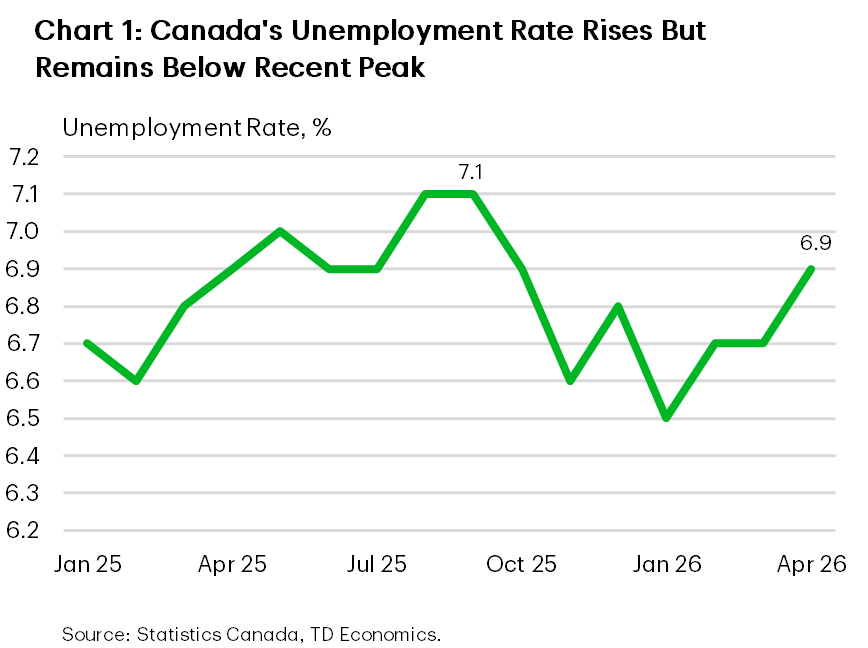

- Canada’s labour market remained soft in April, with employment down and the unemployment rate rising to 6.9%.

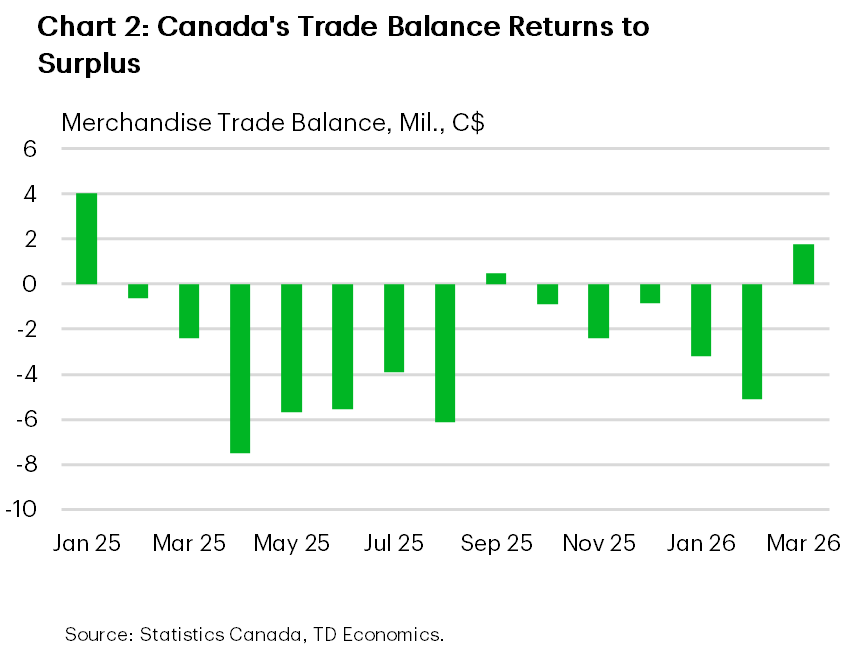

- Canada’s trade balance returned to surplus in March on stronger commodity exports, though net trade is still likely to subtract from Q1 GDP growth.

- A soft labour market and weak ex-energy trade should keep the Bank of Canada in a wait-and-see mode despite energy prices.

U.S. Highlights

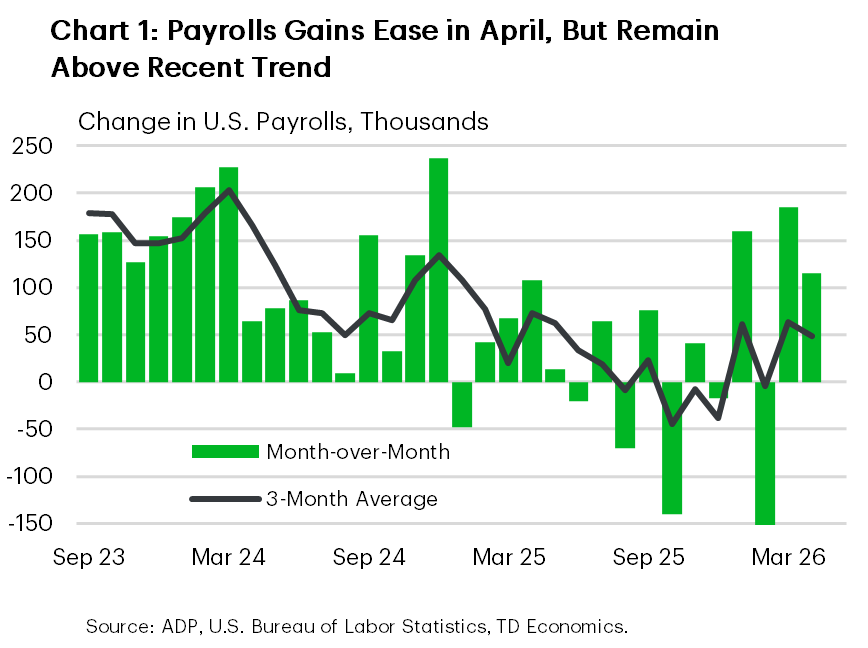

- U.S. payroll growth was solid in April, defying market expectations, while the unemployment rate held steady at 4.3%.

- Historically lean jobless claims reaffirmed a muted environment for layoffs, while the ISM Services Index signaled continued expansion in the services side of the economy.

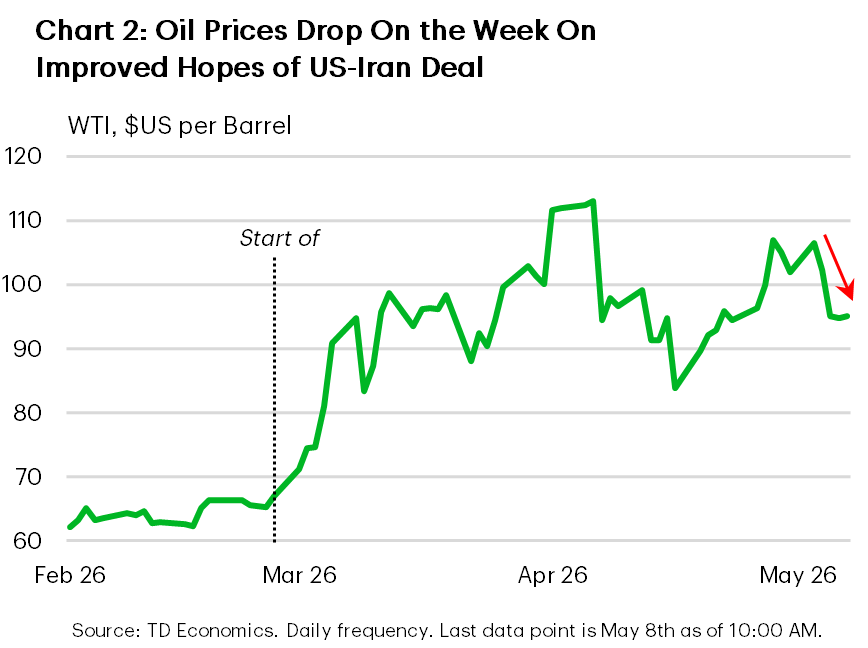

- Volatility in oil prices continued this week as WTI crude oil retreated from $105 per barrel to the mid-$90s later in the week on hopes of a breakthrough in U.S.-Iran negotiations.

Canada – More Reason to Wait and See

The price of oil prices slid below $100 this week (WTI benchmark) on optimism surrounding a potential U.S.-Iran deal, helping both bond and equity markets regain their footing. Canada’s S&P/TSX Composite Index rose 0.6% on the week, though the gain was not enough to prevent it from surrendering its position as the world’s seventh-largest equity market to South Korea (the KOSPI). Bond markets also rallied, pushing 5- and 10-year Government of Canada benchmark yields down 9 basis points to 3.5% and 3.1%, respectively.

April’s jobs report provided a softer read on the economy. According to Statistics Canada, employment was little changed in April, declining by 18k versus expectations for a 10k gain, while the unemployment rate edged up to 6.9% (Chart 1). The labour force participation rate ticked up to 65.0%, contributing to the rise in unemployment. The increase in participation could be viewed as a modest positive, with workers being drawn into the labour market often a vote of confidence in job prospects. That said, there was little evidence of broader momentum beneath the surface. Meanwhile, wage growth decelerated in April, with constant-composition measures showing little improvement.

To some extent, this lack of labour market dynamism works in the Bank of Canada’s favour by helping contain broader price pressures from the energy price shock. The Bank has continued to characterize labour conditions as “soft”, reflecting subdued hiring and weaker demand for workers. As such, this report is unlikely to materially alter its current wait-and-see approach.

A similar message came from the trade report. Canada’s trade balance moved back into surplus in March after five consecutive monthly deficits (Chart 2). However, the improvement was largely driven by commodity prices and precious metals rather than broad-based external demand. Export values surged on higher crude oil prices and increased gold shipments, while imports pulled back following February’s outsized gain.

Excluding metal, mineral, and energy products, export growth was far more moderate. As a result, March’s trade report likely overstates the strength of the external sector. We continue to expect net trade to subtract from Q1 2026 real GDP growth, reflecting stronger imports over the quarter. If energy prices remain elevated, nominal exports and the trade balance should improve further in Q2 even if real export volumes remain subdued

Higher energy exports, however, offer little consolation to consumers. Our proprietary card-spending data show gas station spending rising 3.6% on the month and 16.7% on the year in April, before the gas tax holiday took effect, adding pressure to household budgets. The Bank of Canada has indicated it stands ready to respond should higher energy prices feed more broadly into inflation, but for now there is little reason for policymakers to move decisively in either direction.

U.S. – Labor Market Resilient Despite Energy Shock

U.S. financial markets remained firm this week. The S&P 500 advanced roughly 2% to new record highs, supported by a pullback in oil prices and a better-than-expected jobs report. Long-term Treasury yields eased later in the week, with the 10-year note hovering near 4.35% – a hair below last week’s close. Market pricing continues to reflect limited expectations for near-term rate cuts amid ongoing energy market uncertainty and a relatively resilient economy.

Resiliency was on display in the April jobs report, where nonfarm payrolls rose 115,000 – almost double the market consensus forecast. The unemployment rate held steady at 4.3% amid modest declines in both household employment and the labour force. Payrolls were volatile through the first quarter, due in part to factors like inclement weather and a healthcare strike in California. Looking through the volatility, it appears that job growth has picked up from its anemic trend at the end of last year and is now running at a decent pace that’s allowing it to hold the unemployment rate steady (Chart 1). High-frequency indicators reinforced this resilient labour market picture: initial jobless claims remained very low by historical standards, while continuing claims fell to 1.77 million – a new two-year low.

Other economic data lent further support to the resilience theme. The ISM Services Index eased modestly in April but remained comfortably above the 50-point expansion threshold. The details of the report, however, had a few blemishes. New orders recorded a notable pullback, while the prices-paid component remained elevated at 70.7 – the highest level since late 2022 and up notably from earlier this year – pointing to persistent cost pressures in the services sector.

With respect to prices, the good news is that the price of WTI crude oil, which had surged above $105/barrel late last week, fell back to the mid-$90s over the course of this week (Chart 2). This followed reports of U.S.–Iran negotiations and tentative de-escalation signals around the Strait of Hormuz. While constructive for inflation expectations, sustained disinflation will depend on a more durable resolution to the tensions.

These developments are likely front-of-mind for Fed Chair-nominee Kevin Warsh as he prepares to take the helm. Communication from the Fed this week maintained a cautious stance, with New York Fed President John Williams emphasizing that policy is “well positioned” to balance the risks to the dual mandate. Under the current backdrop, market odds remain strongly in favor of no Fed action over the near term, with the probability that rates are held steady this year still sitting at over 70%. Ultimately, this morning’s better-than-expected jobs report, alongside other high-frequency indicators, helps ease concerns that the U.S. labour market has continued to deteriorate. This should give policymakers more breathing room to assess the extent to which higher energy prices filter into core inflation over the coming months.