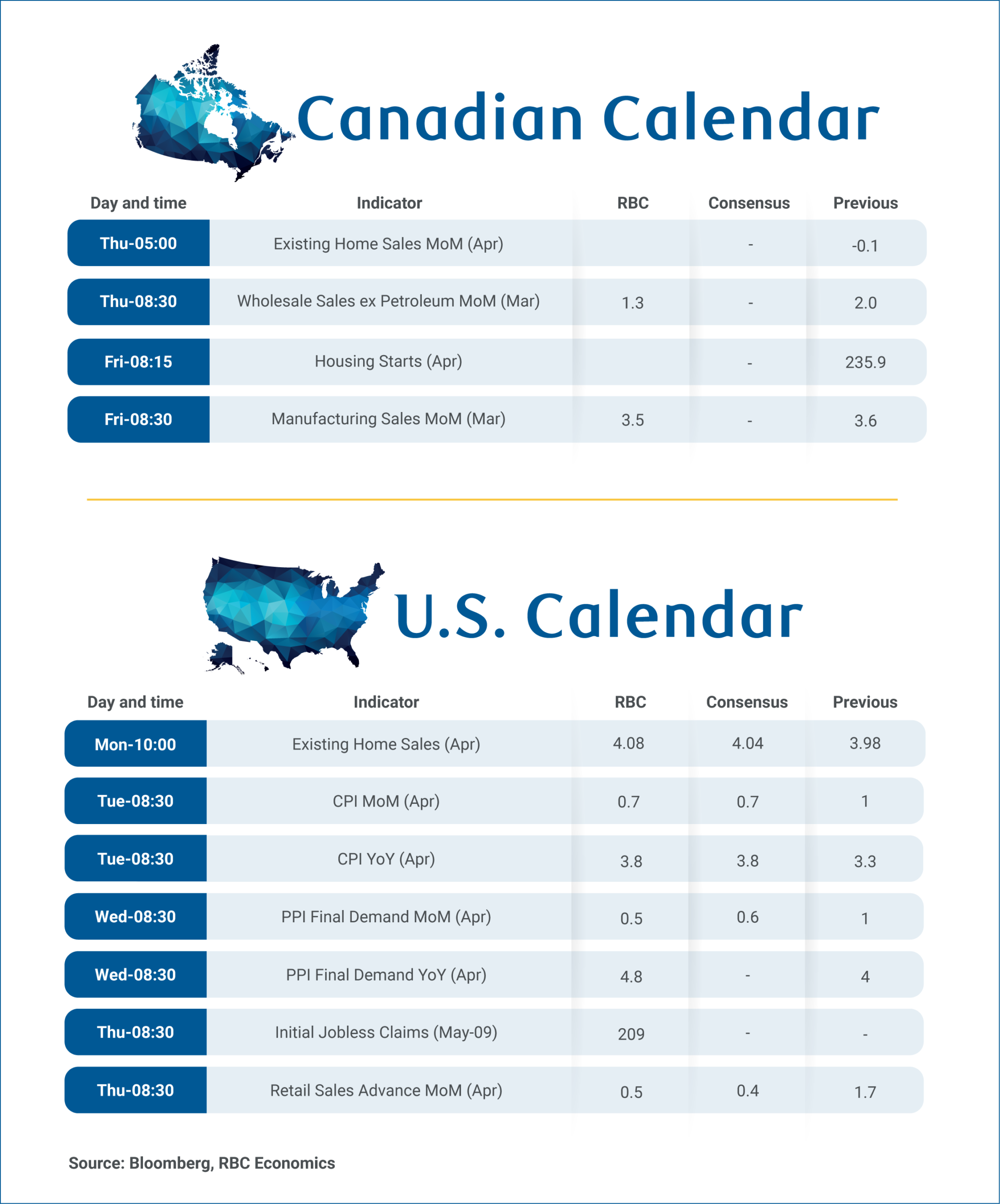

The week ahead is relatively quiet for major Canadian data releases, but industry reports will offer important signals about the economy’s momentum heading into spring.

Early signs from Statistics Canada’s advance estimates suggest wholesale trade for April on Thursday and manufacturing sales next Friday should show the sectors finding their footing after significant disruptions to motor vehicle production earlier in the year.

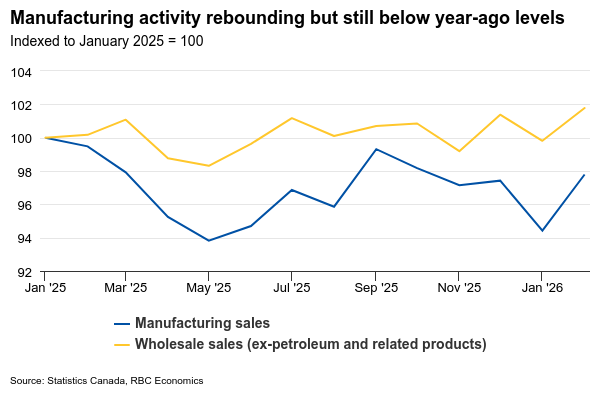

Early estimates showed March manufacturing sales rising 3.5%, lifted by the petroleum and coal product subsector as energy prices surged amid escalating Middle East conflicts, along with further recovery in the transportation sector. Separately reported data from the Industrial Product Price Index suggests about half the increase was due to higher prices, but that would still leave ‘real’ sales up about 1.7%.

This is significant, because the sector has been under pressure. As of February, manufacturing was still running below levels a year ago, weighed down by product specific tariffs on products like steel and aluminum as well as the motor vehicle sector. Yet, recent data points to a steadying trend. Both trade flows and manufacturing output have shown signs of stabilization, and U.S. tariffs have been broadly edging lower.

Wholesale trade tells a similar story. The advance indicator showed core sales (which exclude the price-related increases in petroleum and related products) rose 1.3% in March.

Housing data for April will also be released next week. Early results from local real estate boards show more sellers entering the market, with new listings reaching record levels in Montreal and Ottawa. Home resales rose month-over-month in Toronto (up 6.1%), Calgary and Edmonton, though remained weaker year-over-year in most markets. Buyers continue to hold stronger negotiating power in Vancouver and Toronto where ample inventory is sustaining price corrections—Toronto’s MLS HPI fell 6.5% year-over-year while Vancouver’s dropped 6.9%. The spring season has yet to deliver a clear boost to demand, with confidence constrained by trade uncertainty, job market concerns and affordability challenges.

South of the border, U.S. consumer prices data for April are expected to show headline inflation ticking higher to 3.8% year-over-year, driven by rising gasoline prices. Core inflation, which strips out volatile food and energy categories, is expected to remain more subdued, edging to 2.7% year-over-year.

U.S. retail sales are expected to tick up 0.5% in April, decelerating from the robust 1.7% in the prior month. Unit auto sales posted a decline in April following two consecutive months of growth, but that was offset by higher sales at gas stations due to higher prices.